ATR Volatility Trading & Position Sizing

Master Average True Range (ATR) for volatility-based position sizing and stop loss placement. Learn how to adapt your trading to market volatility for consistent risk management.

What is ATR?

Average True Range (ATR), developed by J. Welles Wilder, measures market volatility by calculating the average range between high and low prices over a period (typically 14 days). Unlike other indicators that predict direction, ATR only measures volatility - how much a stock moves.

ATR is crucial for position sizing and stop loss placement. A stock with $5 ATR needs wider stops than one with $1 ATR. By using ATR, you normalize risk across different stocks regardless of their volatility.

Key Insight: ATR doesn't predict direction - it measures how much a stock typically moves. Use it for risk management, not entry signals.

ATR Formula

Step 1: Calculate True Range (TR)

1. Current High - Current Low

2. |Current High - Previous Close|

3. |Current Low - Previous Close|

Example: High $105, Low $100, Prev Close $102

- Option 1: $105 - $100 = $5

- Option 2: |$105 - $102| = $3

- Option 3: |$100 - $102| = $2

- TR = $5 (maximum)

Step 2: Calculate ATR (14-period)

Subsequent ATR = [(Prior ATR × 13) + Current TR] / 14

Smoothed moving average that adapts to recent volatility

Why True Range?

True Range accounts for gaps:

- Gap Up: High - Prev Close captures full move

- Gap Down: Prev Close - Low captures full move

- No Gap: High - Low is sufficient

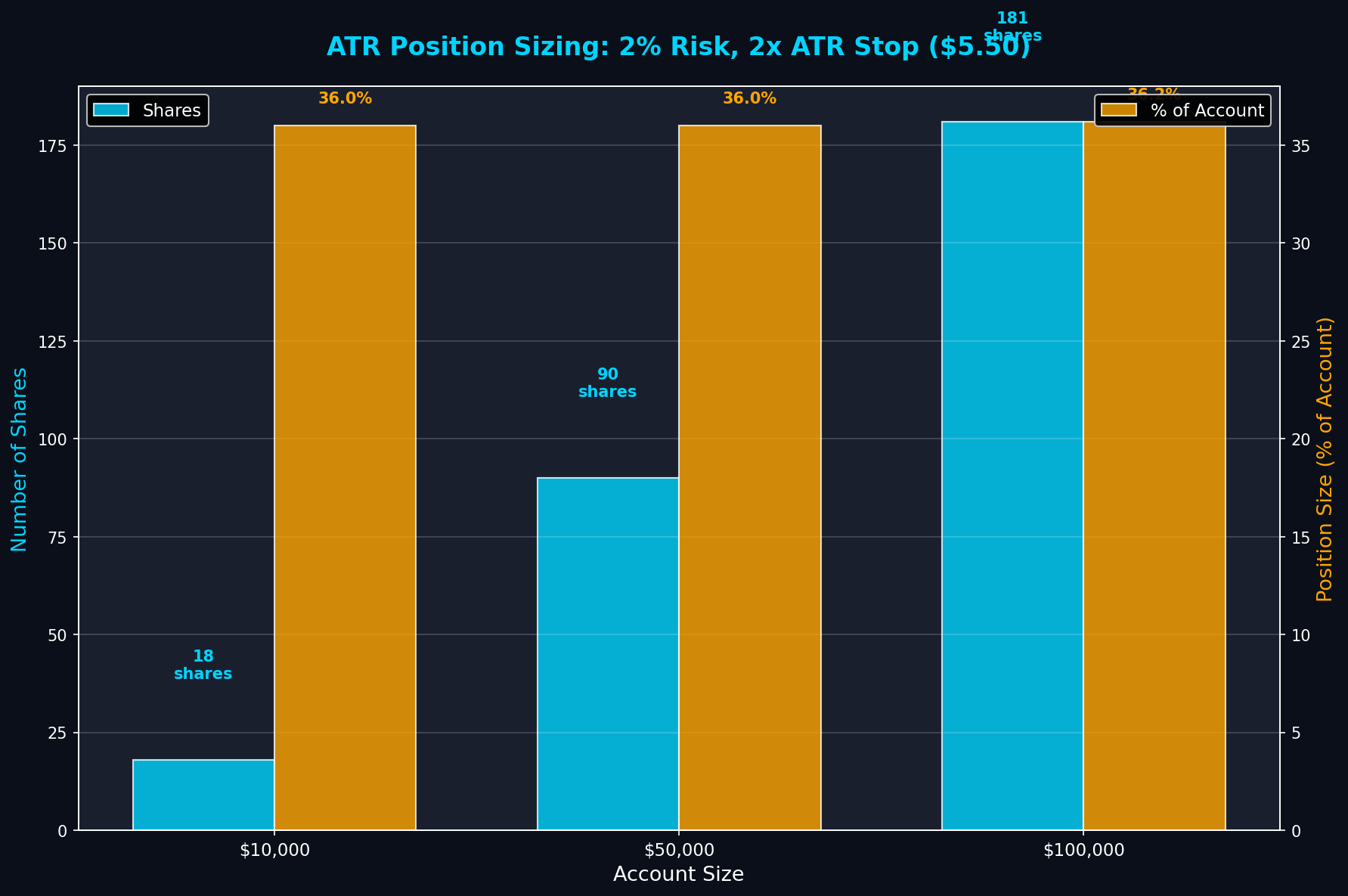

ATR-Based Position Sizing

The most important use of ATR - sizing positions based on volatility:

Position Sizing Formula

Example: $100k account, 2% risk, ATR $5, 2x multiplier

- Risk Amount: $100,000 × 0.02 = $2,000

- Stop Distance: $5 × 2 = $10

- Shares: $2,000 / $10 = 200 shares

- Position Value: 200 × $200 = $40,000 (40% of account)

ATR Multipliers

- 1x ATR: Tight stop, higher risk of stop-out, larger position

- 2x ATR: Standard stop, balanced approach (recommended)

- 3x ATR: Wide stop, lower risk of stop-out, smaller position

- 4x ATR: Very wide stop, swing trading, smallest position

Trading Rule: Use 2x ATR for day trades, 3x ATR for swing trades. This gives price room to breathe while protecting capital.

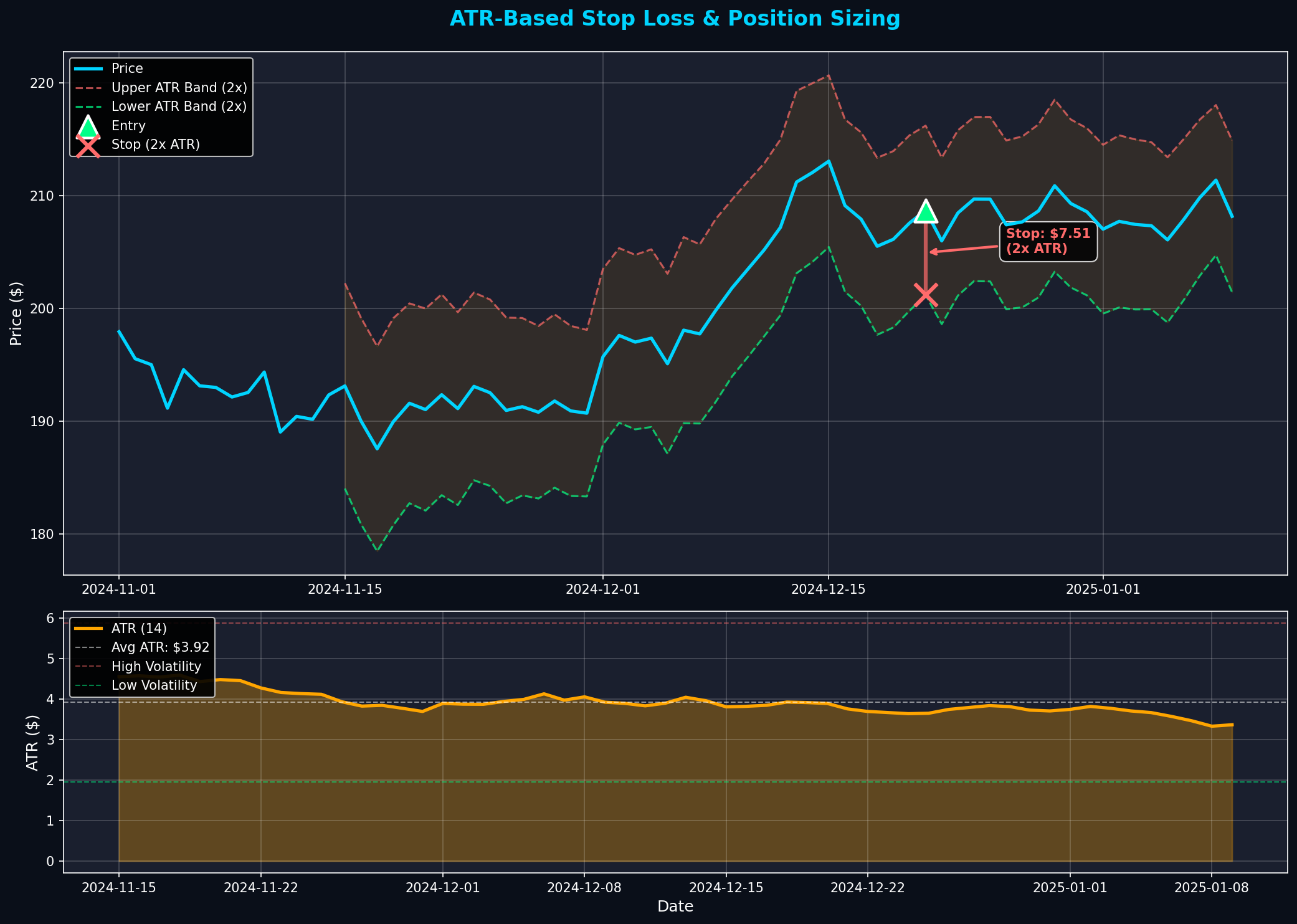

ATR Stop Loss Strategies

1. Initial Stop Loss

Long Position:

Example: Entry $100, ATR $5, 2x multiplier

Stop = $100 - ($5 × 2) = $90

2. Trailing Stop Loss

As trade moves in your favor:

Recalculate daily as ATR changes

- ATR increases (more volatile) = wider stop

- ATR decreases (less volatile) = tighter stop

- Never lower stop, only raise it

3. Chandelier Stop

Trail from highest high:

Hangs down from ceiling (highest high) like a chandelier

Volatility Expansion/Contraction

Low ATR (Contraction)

- Meaning: Low volatility, consolidation, coiling

- Signal: Big move coming (direction unknown)

- Action: Prepare for breakout, tighten stops

- Position Size: Can be larger (lower risk per share)

High ATR (Expansion)

- Meaning: High volatility, trending or panic

- Signal: Move in progress, potential exhaustion

- Action: Widen stops, trail aggressively

- Position Size: Must be smaller (higher risk per share)

ATR Percentile Analysis

Compare current ATR to 6-month range:

- ATR < 25th percentile: Extremely low volatility, breakout imminent

- ATR 25-75th percentile: Normal volatility

- ATR > 75th percentile: High volatility, reduce position size

- ATR > 90th percentile: Extreme volatility, avoid new positions

Trading Strategies

Strategy 1: Volatility Breakout

- Wait for ATR to drop below 25th percentile (low volatility)

- Identify consolidation pattern (range, triangle, flag)

- Enter on breakout with volume

- Stop: 2x ATR below entry

- Target: 3-5x ATR from entry

Strategy 2: ATR Trailing

- Enter trend-following trade (any method)

- Set initial stop at 3x ATR

- Trail stop daily: Price - (3x Current ATR)

- Exit when price hits trailing stop

- Captures full trend, exits on volatility spike

Strategy 3: Volatility Filter

- Only trade stocks with ATR 2-6% of price

- Too low (< 2%) = not enough movement

- Too high (> 6%) = too risky

- Sweet spot: 3-4% ATR for swing trading

Common Mistakes

- Fixed Dollar Stops: Using $5 stop for all stocks ignores volatility. Use ATR-based stops instead.

- Same Position Size: Buying 100 shares of every stock ignores risk. Size based on ATR.

- Too Tight Stops: Using 1x ATR gets stopped out by normal noise. Use 2-3x ATR.

- Ignoring ATR Changes: ATR changes daily. Recalculate stops regularly.

- Using ATR for Direction: ATR measures volatility, not direction. Don't use it for entry signals.

Key Takeaways

- •ATR measures volatility (how much stock moves), not direction

- •Use ATR for position sizing: Risk $ / (ATR × Multiplier) = Shares

- •Standard stop: 2x ATR for day trades, 3x ATR for swing trades

- •Trail stops using current ATR - adapts to changing volatility

- •Low ATR = consolidation, big move coming (breakout setup)

- •High ATR = trending or panic, reduce position size

- •Normalize risk across stocks by using ATR-based sizing

Get ATR-Based Position Sizing

MarketDly calculates optimal position sizes using ATR for consistent risk management across all trades.

View Pricing PlansReady to Put This Into Practice?

Join MarketDly to access real-time market insights, AI-powered analysis, and professional trading tools.

No credit card required • Free tier available • Upgrade anytime